History

In 2020, I started Pecan Tree Oil & Gas with the mission to bring top-notch engineering to a part of the industry that was largely ignored by the engineering firms (the mineral space).

My formal training as a petroleum engineer providing economic valuations and reserve estimates for large companies taught me all the right ways to solve the problem, and I knew anyone who owned oil and gas property would benefit from the type of service I could provide.

How we can help

But the issue of how to economically provide high-dollar engineering to clients only willing/able to pay a minimal amount was a tough nut to crack. It would have been easy to only do work for high-net-worth clients and funded companies and never look back, but the challenge and need gnawed at me.

There are MILLIONS of mineral owners out there with just small slivers of land that needed valued, and I was getting requests right and left for help. There HAD to be a solution to this.

To be honest, I did a LOT for free. Probably too much. It took a long time to realize even the best of intentions need to be financially stable propositions, and pro-bono work only made sense if MOST of my time was spent on paying work (and it wasn’t). If I wanted to keep doing the work I felt driven to perform for small interest owners, I needed to engineer a better method.

One thing was clear when I started out creating this model: the best way to provide high-quality engineering at the lowest cost possible was to be super, super efficient. Creation of the model was initially an exercise in efficiency. I needed a way to automate as much as possible and re-use as much analysis as possible. I did what any good engineer does and created an overly complex Excel file to do the analysis, then created a database to house the well and map data.

Years and years of trial and error later, the current model was born. It’s grown quite a bit from its humble Excel beginnings.

The Model

At its core, the model is a collection of equations and assumptions used to calculate the value of any plot of land based on the data specific to that location.

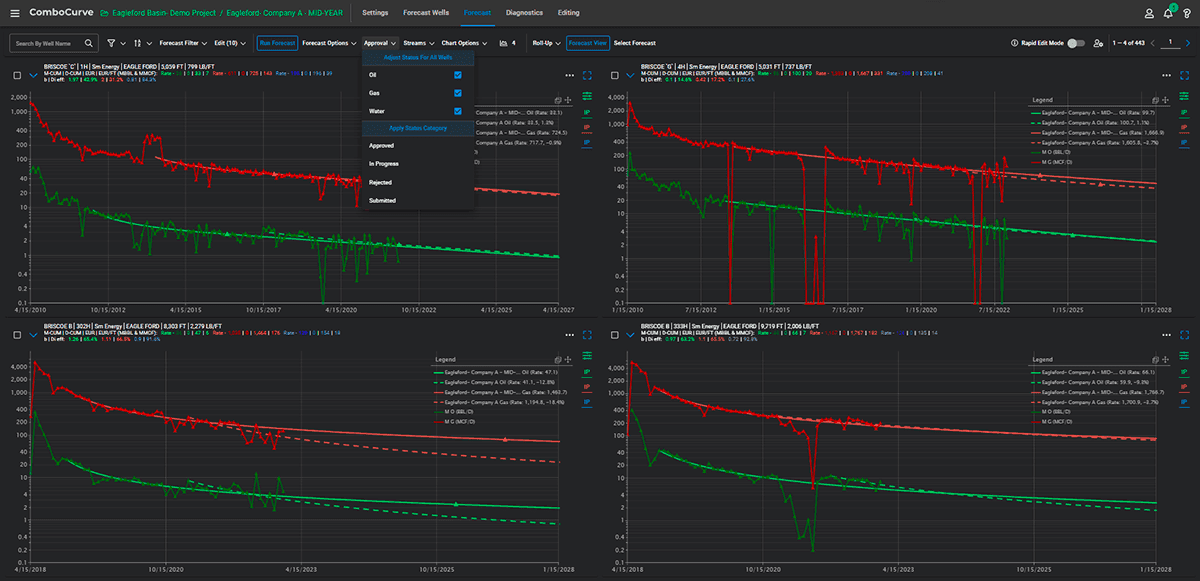

Some of that data is proprietary, but much of it is public. Some of those equations are off the shelf solutions like ComboCurve for our economic modeling, and some of the equations are made in-house using data-driven approximations.

Engineering Valuation Model

Pecan Estimate

Geology & Engineering

Decline Curve & Type Wells

Estimated Ultimate Recovery

Reserve Analysis (3P)

GIS Mapping

Appraisal Methods

Discounted Cash Flow

Income / Lease Bonus Multiples

Comparative Sales

USPAP

Market Inputs

Society of Petroleum Evaluation Engineers

Buyer / Seller Feedback

NYMEX Commodity Futures

Propriety Data

Aggregated & anonymous client-submitted data

In-House Data Analysis & Models

Public Data

Wells, Production, Filings, Permits, Rigs, Locations (WellDatabase)

Tax Appraisal Data

Investor Presentations

Engineering Methods

In 2020, I started Pecan Tree Oil & Gas with the mission to bring top-notch engineering to a part of the industry that was largely ignored by the engineering firms (the mineral space).

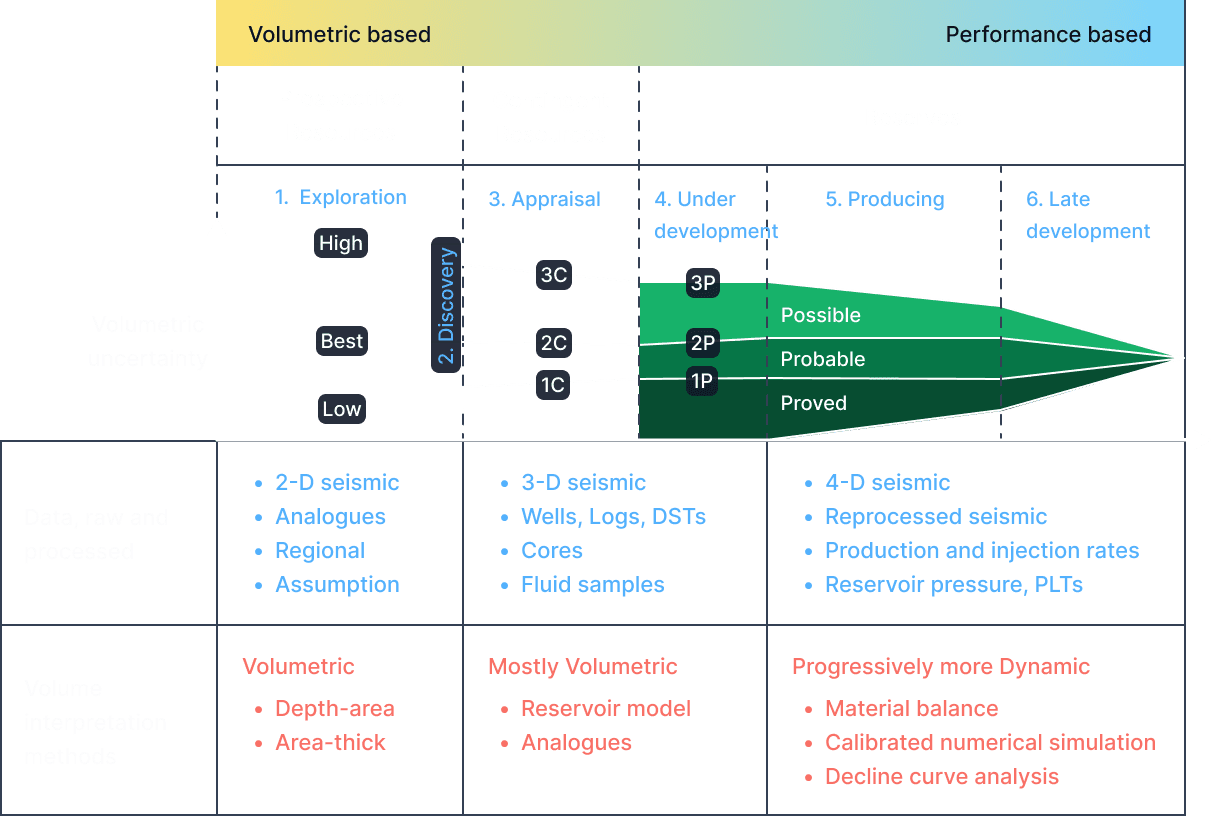

To establish proven reservoir in an unconventional play, the proximity and density of development of the reservoir is used.

Acreage in a reservoir is deemed “proven” if there is established production within a certain radius in the same reservoir.

Type curves are created to estimate the amount recoverable from a certain area given a certain number of wells draining an area.

This is all done in harmony with Decline Curve Analysis to forecast production on existing wells. This is consistent with the type curve methodology outlined in SPEE Monographs 3 and 4.

As of right now, we have about 185,000 wells in our ComboCurve and ~415 unique type curves.

There are a lot of methods that can be used to estimate remaining recoverable oil and gas, but MOST of the onshore USA uses Decline Curve Analysis for producing wells, and analogy for undrilled and newly-drilled wells.

Exceptions to this would be waterfloods, CO2 floods, new vertical wells, and reservoirs with a significant aquifer providing energy (which is a lot of the Gulf Coast sand reservoirs).

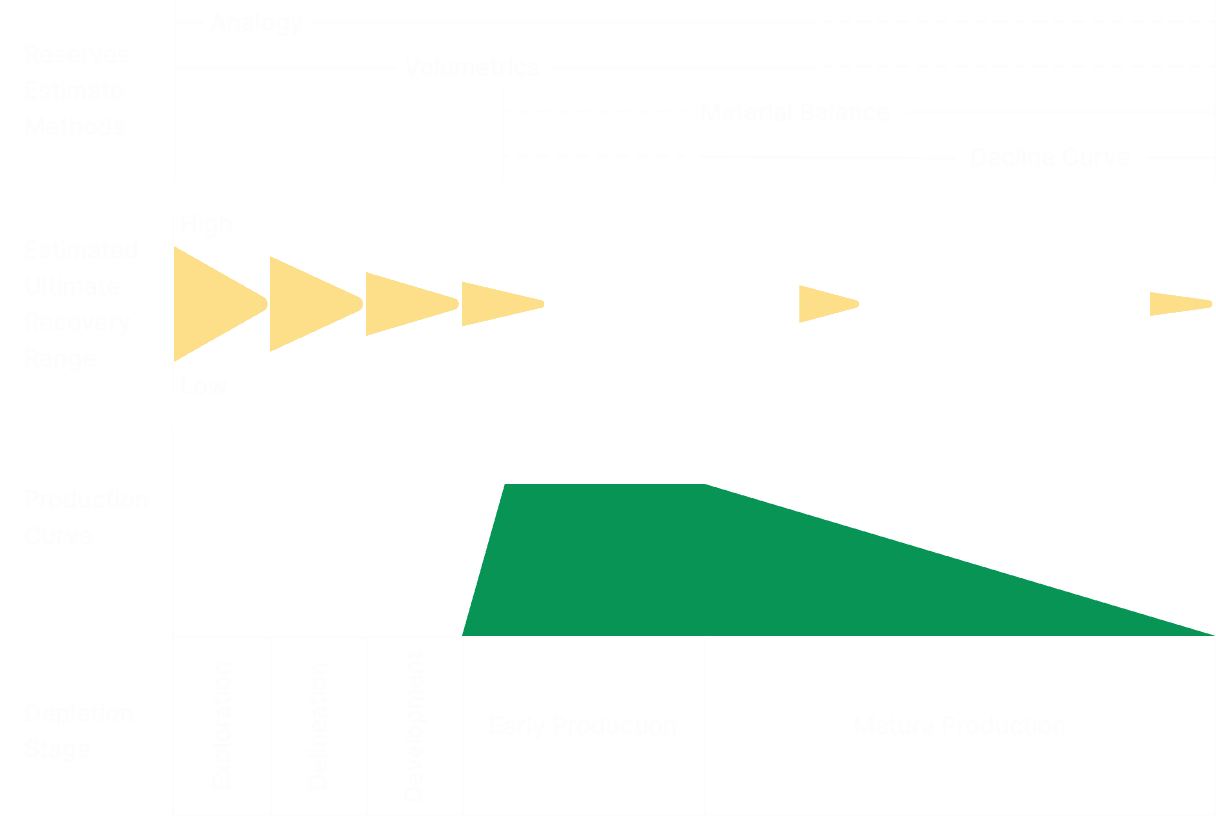

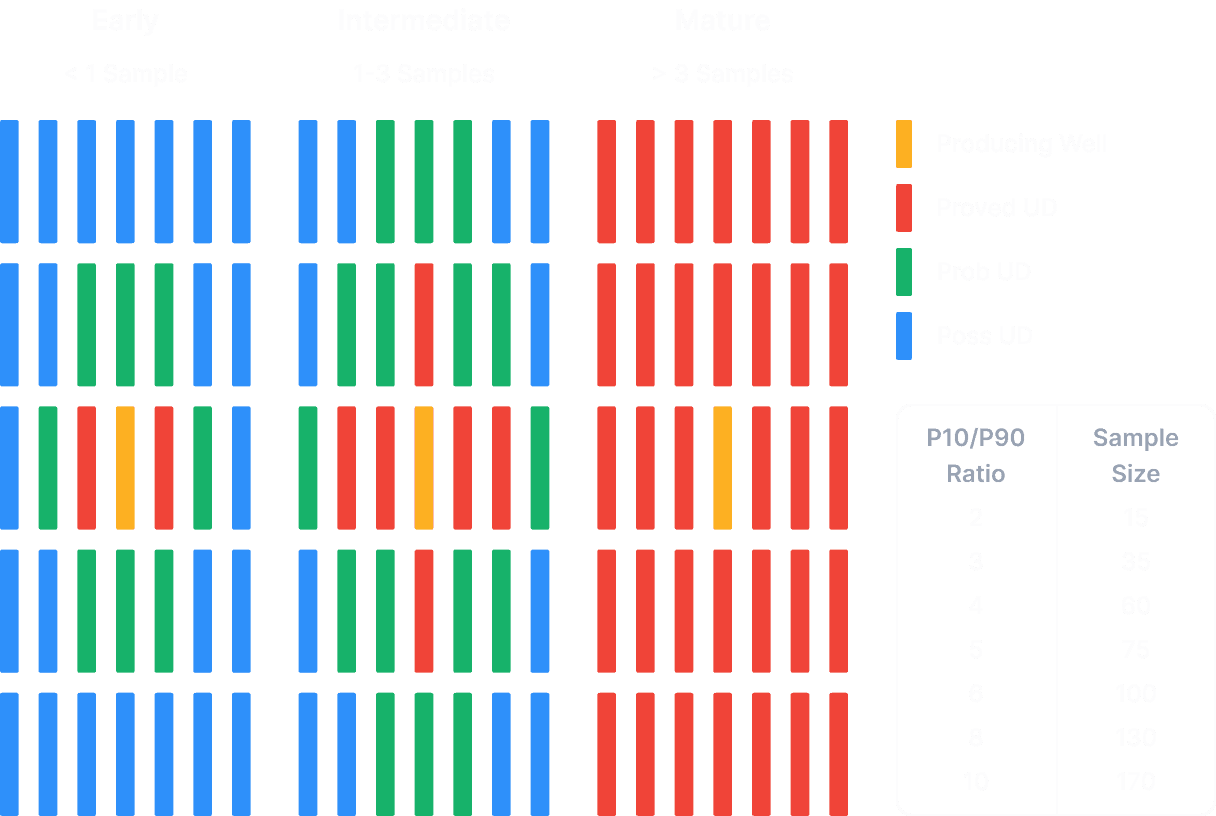

When the reservoirs of value are largely unconventional shale, we can use analogy methods and use the maturity of surrounding development to statistically quantify how much of a reservoir is considered proved, probable, and possible.

How much is proven is highly determined by the variability between wells in the area, or a P90/P10 ratio (aka, how much spread is there between the best and worst wells in the sample set, and how big is the sample set).

As an area matures from initial exploration to development, the certainty of how much oil and gas is recoverable gets more narrow.

Certainty = Value. Uncertainty = Risk.

*Graph for illustrative purposes only. Note that resources or reserves may increase, decrease or remain constant over time. Final produced volume could be within or outside the ranges defined in each stage.

Proximity Method

When there are no reserves (producing or undeveloped) in an area to value using an engineering cash flow analysis, our model uses a proprietary proximity model which looks at the value and activity in the surrounding 20 miles.

This method accounts for the intrinsic value of minerals being higher when closer to known reserves, but is not a formal industry method.

For example, property in an area that has more production around it will have simply due to the potential for future discoveries. Intrinsic value extends beyond quantifiable measurements but is intended to encompass the inherent worth of a property.

This value is speculative and does not account for any technological or geological developments that may not yet be public knowledge.

Prior to these developments becoming public and then built into our model, this intrinsic value method captures production from new wells to influence the surrounding value of an area.

The Hex Grid

There is a hexagonal grid that underlies the model as a backbone of structure. Each grid is about 1 mile in diameter and all of the “heavy lifting” equations of the reserve volumes explained above are done at this level.

Each grid, for example, has which reservoirs are present at that grid and the % PDP, PDNP, PDSI, PUD, PROB, and POSS for that reservoir in that grid.

For the whole country. It’s as complicated of a script to run as it seems it would be, so this is all done ahead of time whenever the engineering interpretations are updated for an area.

This leaves us with a somewhat solved answer of how much oil and gas is remaining in each grid, but doesn’t answer the question of what any one specific property is worth. For this, we employ more code to compare the area drawn to the underlying grids and customize the solution even further to account for the units created, the positioning of the wells within the grids, and other items unique to the property.

Luckily this part is relatively quick since the heavy lifting was already completed, so the tool can run these equations on the fly whenever a user inputs a new property request. The output is our Pecan Estimate.

Appraisal Guidelines

I also was VERY sensitive to maintaining the public trust in the word “appraisal” as a Certified Mineral Appraiser.

You’ll never see the word appraisal used here unless it’s referring to appraisals that follow the USPAP recommended methods.

While the Pecan Estimate is a superb approximation tool, it should be used as a starting point and is not a replacement for detailed, technical appraisals that would be needed for Capital Gains calculation, estate tax basis, or other formal uses.

Commodity Pricing

Future commodity prices are projected using the NYMEX posted future pricing of Crude Oil (WTI) and Natural Gas (Henry Hub).

The value is then held flat for the remainder of the model. NGLs are priced at % of WTI Crude Oil pricing based on the trailing-twelve-month average blend of products approximating an NGL blend (45% Henry Hub Natural Gas, 25% Mont Belvieu propane, 25% Gulf Coast gasoline, and 5% WTI crude oil).

Basin-specific differentials are deducted from WTI Index pricing to account for API gravity and other regional adjustments. Similarly, a basin-specific differential is applied to Henry Hub natural gas to adjust for regional hub pricing vs Henry Hub. An additional deduction is applied for gathering, processing, and other fees and considered “post-production costs.”

References

Production data, permits, rig location, and well status data sourced from WellDatabase.com

NYMEX crude oil futures sourced from https://www.investing.com/commodities/crude-oil-contracts

NYMEX natural gas futures sourced from https://www.investing.com/commodities/natural-gas-contracts

Appraisal Standards Board. 2020. Uniform Standards of Professional Appraisal Practice. 2020–2021 ed. The Appraisal Foundation.

Society of Petroleum Engineers. 2018. Petroleum Resources Management System. https://www.spe.org/en/industry/reserves/.

SPE Oil & Gas Reserves Committee. 2007. “SPE/WPC/AAPG/SPEE Petroleum Resources Management System (PRMS).” 2007.

https://www.spe.org/industry/docs/PRMS-Process-2007.pdf.

Society of Petroleum Evaluation Engineers. 2023. “Annual Survey of Parameters Used in Property Evaluations.” Presented at the Annual Meeting of the Society of Petroleum Evaluation Engineers.